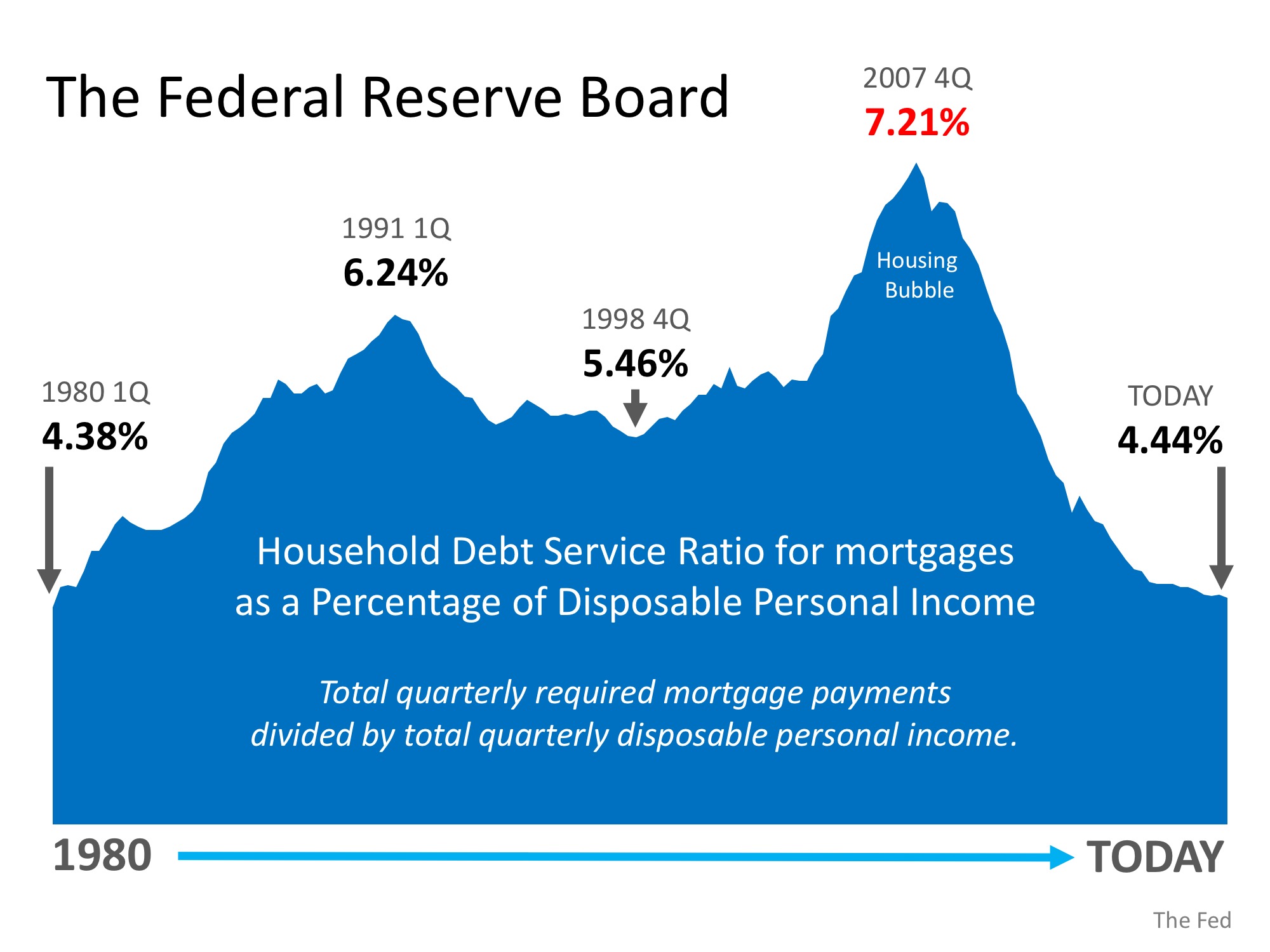

There are many unsubstantiated theories as to why home values are continuing to increase. From those who are worried that lending standards are again becoming too lenient (data shows this is untrue), to those who are concerned that prices are again approaching boom peaks because of “irrational exuberance” (this is also untrue as prices are not at peak levels when they are adjusted for inflation), there seems to be no shortage of opinion.

However, the increase in prices is easily explained by the theory of supply & demand. Whenever there is a limited supply of an item that is in high demand, prices increase.

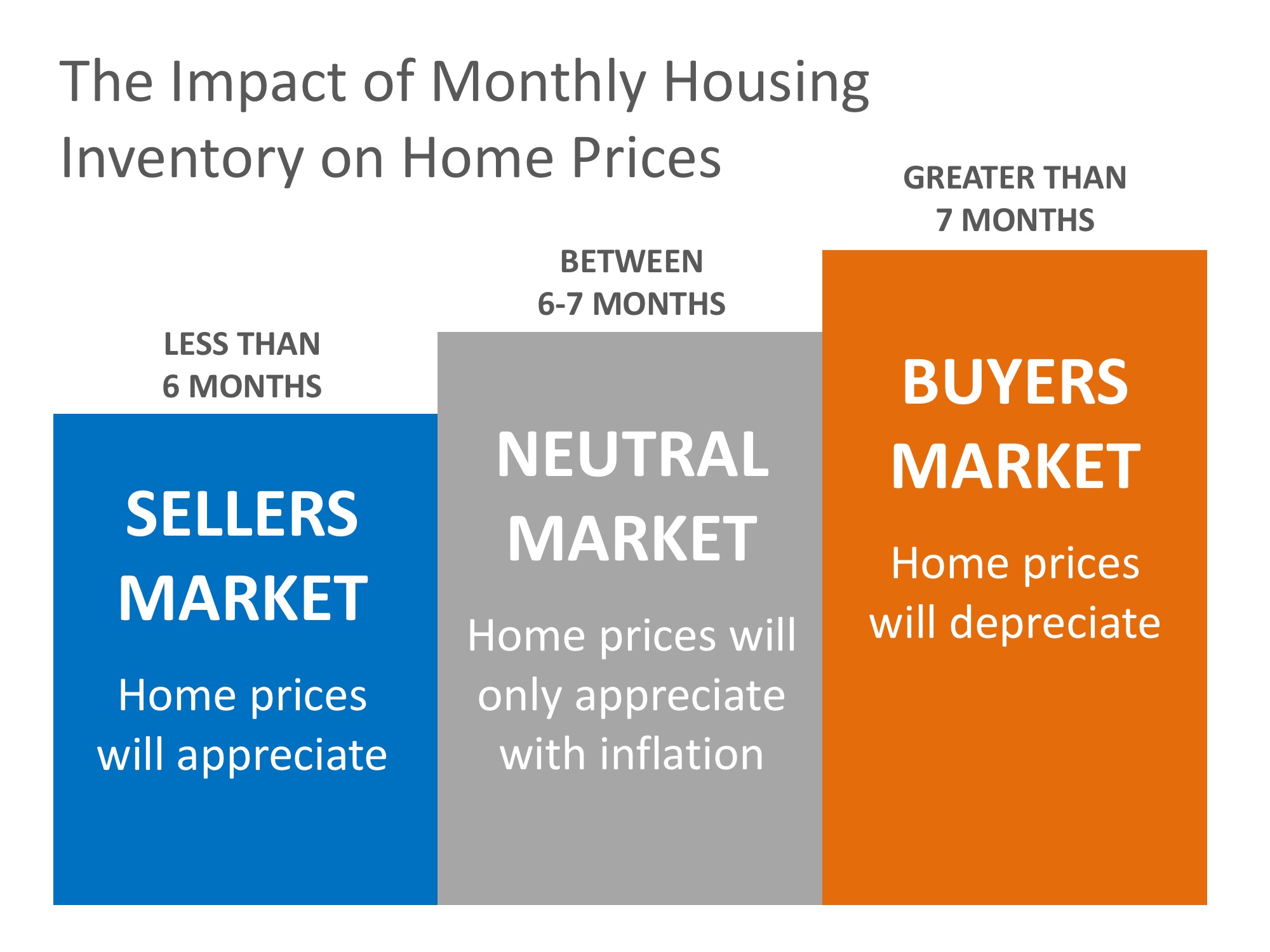

It is that simple. In real estate, it takes a six-month supply of existing salable inventory to maintain pricing stability. In most housing markets, anything less than six months will cause home values to appreciate and anything more than seven months will cause prices to depreciate (see chart below).

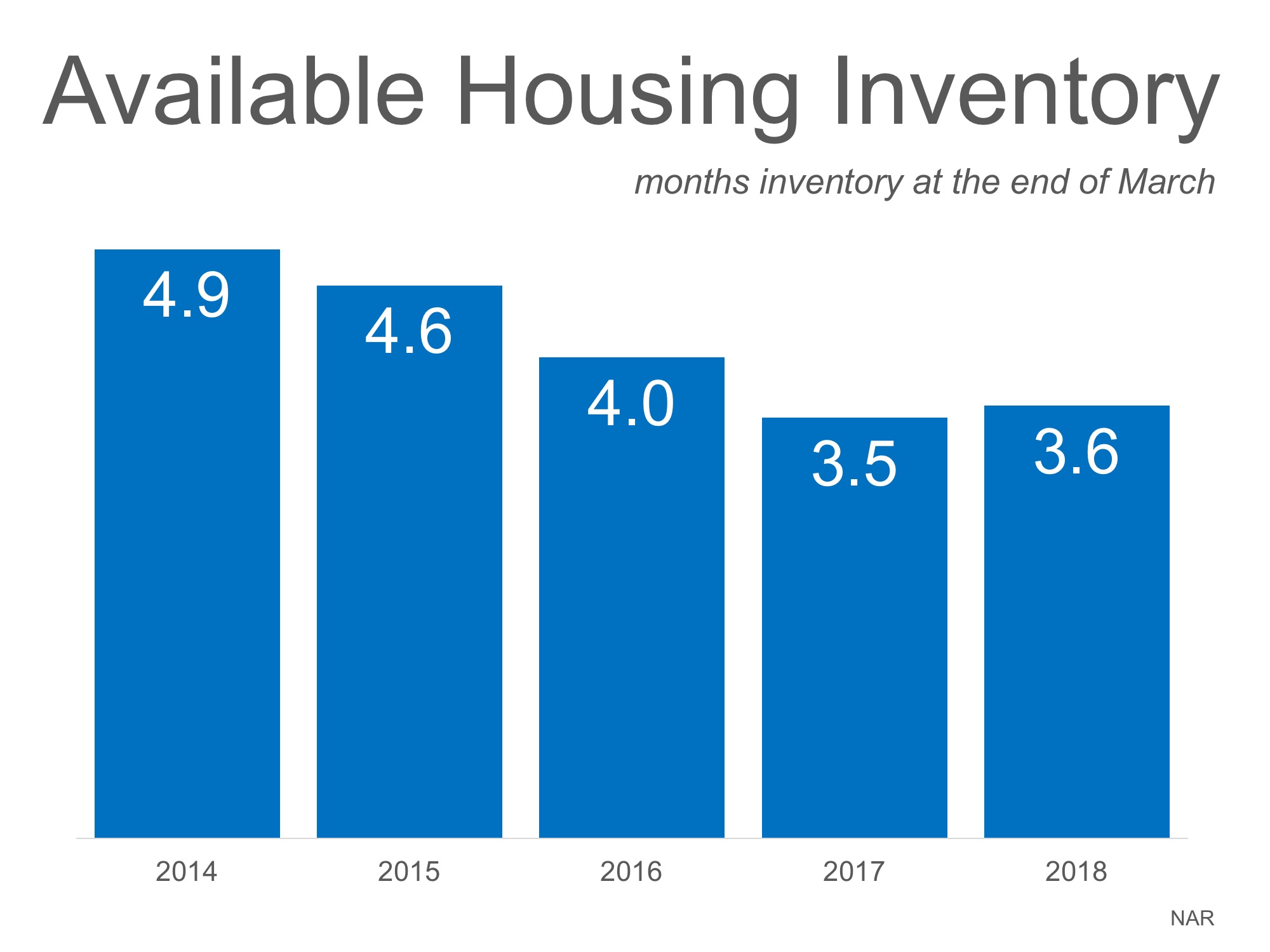

According to the Existing Home Sales Report from the National Association of Realtors (NAR), the monthly inventory of homes for sale has been below six months for the last five years (see chart below).

Bottom Line

If buyer demand continues to outpace the current supply of existing homes for sale, prices will continue to appreciate. Nothing nefarious is taking place. It is simply the theory of supply & demand working as it should.

from Simplifying the Market™ https://ift.tt/2r8uUdh

via IFTTT

![Existing Home Sales Grow Despite Low Inventory [INFOGRAPHIC] | Simplifying the Market](http://files.simplifyingthemarket.com/wp-content/uploads/2018/04/24163655/20180427-Share-STM.jpg)

![Existing Home Sales Grow Despite Low Inventory [INFOGRAPHIC] | Simplifying the Market](http://files.simplifyingthemarket.com/wp-content/uploads/2018/04/24163629/20180427-EHS-Report-STM-ENG.jpg)

![Home Buying Myths Slayed [INFOGRAPHIC] | Simplifying the Market](http://files.simplifyingthemarket.com/wp-content/uploads/2018/04/19123027/20180420-Share-STM.jpg)

![Home Buying Myths Slayed [INFOGRAPHIC] | Simplifying the Market](http://files.simplifyingthemarket.com/wp-content/uploads/2018/04/19122954/20180420-STM-ENG.jpg)